India’s economy appears resilient against the recent surge in U.S. tariffs, according to a report released by Moody’s Ratings. While the agency anticipates only minor repercussions from these trade barriers, it cautions that ongoing global trade disputes may impede economic growth and credit conditions on a worldwide scale. GDP growth in India is projected to slightly decline to 5.5%–6.5% in 2025, a revision from the previous estimate of 6.6%.

Global Trade Tensions and India’s Economic Outlook

The downgrade in growth expectations is largely linked to a decrease in global demand and a slowdown in merchandise exports, particularly toward the United States. Notably, India’s exports to the U.S. represent 6.6% of its nominal GDP, indicating a moderate level of exposure to the U.S. administration’s protective trade policies.

- Exports to the U.S.:

- Represent 6.6% of nominal GDP

- Increased trade surplus: $41.18 billion in FY25, up from $35.32 billion the previous year

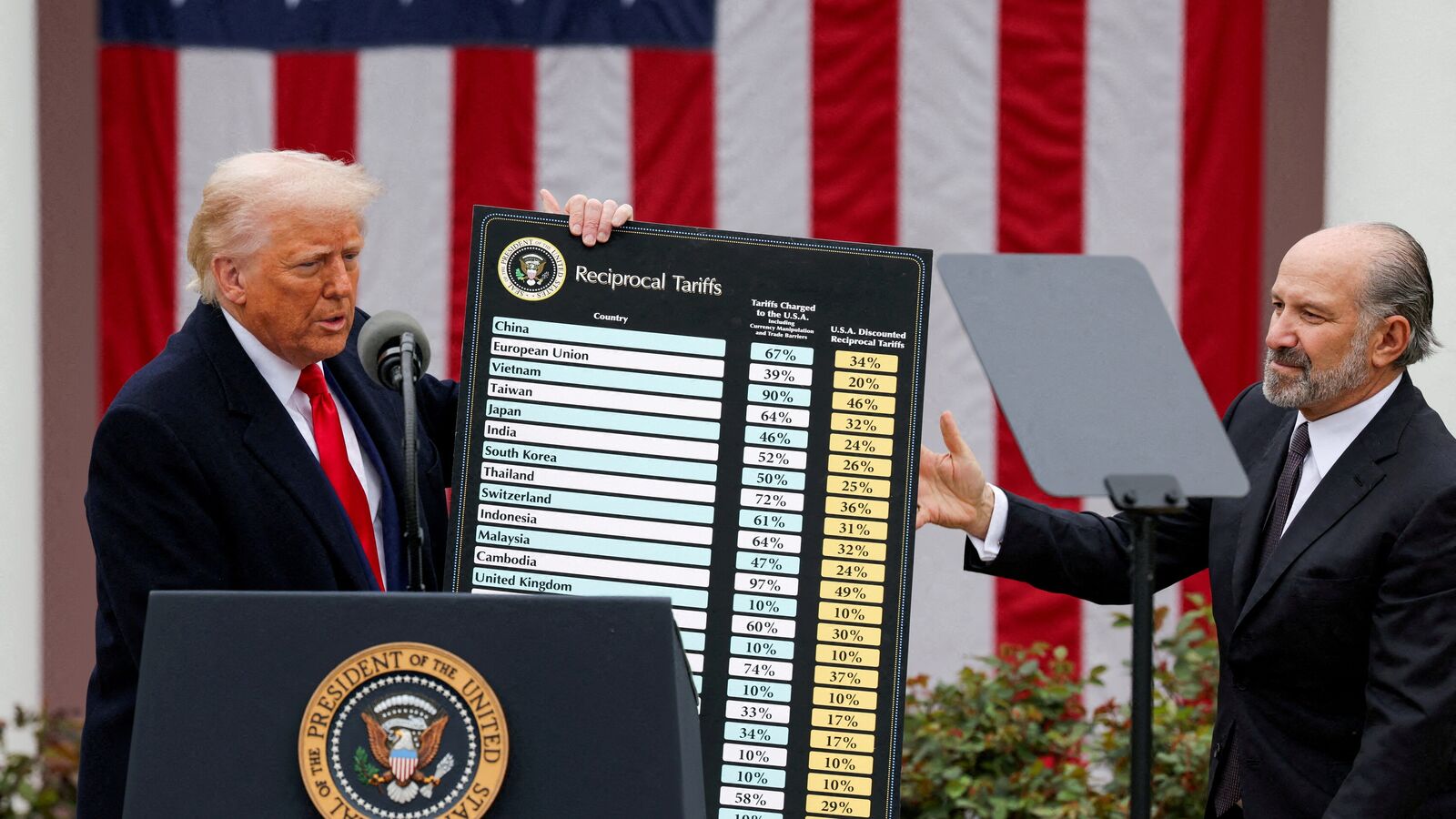

This trade surplus saw a notable 16.6% increase in the last financial year, showcasing India’s growing market advantage. Meanwhile, President Donald Trump raised tariffs on Indian exports to 27% as of April 2, 2023, citing concerns over the U.S. trade deficit before instituting a temporary pause on tariff hikes on April 9.

India vs. Other Asian Economies

Moody’s analysis indicates that India is better positioned than other significant Asian manufacturing nations such as China, Taiwan, and South Korea in light of the new tariffs. For example, China’s growth could plummet to 4% or lower due to these trade tensions.

Despite India’s relatively stable footing, the report highlights potential fragility in the credit environment. Higher trade barriers could slow down global trade and investment, leading to broader economic consequences.

Implications of U.S. Tariff Policies

Moody’s emphasizes that the new U.S. tariff framework could create substantial turbulence in global markets, potentially tightening credit availability. Even with a pause in tariff hikes, the 145% duty on Chinese goods and a 10% blanket rate on other imports are likely to dampen investment sentiment and push up consumer prices. The agency warns of a potential rise in default rates across various sectors, indicating that economic pressures may increase.

- Key Risks Identified:

- Direct trade exposure

- Macroeconomic weaknesses

- Financial market tightening

Lower-income households may especially feel the impact, with disposable incomes for the bottom third projected to drop more than 4%. Furthermore, American consumers are now facing an average effective tariff burden of 27%, which could lead to price increases of up to 3% soon.

Business Adjustments and Future Challenges

As companies utilize the 90-day pause to reevaluate their supply chains, uncertainty looms beyond this window. Moody’s reports that tighter financial conditions—characterized by widening bond spreads and declining stock prices—could hinder lower-rated firms’ ability to refinance their debts.

While the current tariff regime has been moderated from initial proposals, it remains more restrictive than anticipated, causing retaliatory measures from countries like China. Moody’s anticipates that persistent shifts in global trade policies may necessitate future revisions in credit ratings, highlighting the need for vigilance among policymakers and businesses alike.